On Wednesday, the Securities and Exchange Commission adopted a rule requiring the national securities exchanges and national securities associations to prohibit the listing of any equity security of an issuer that is not in compliance with the compensation committee and compensation adviser requirements in Section 10C of the Securities Exchange Act of 1934.

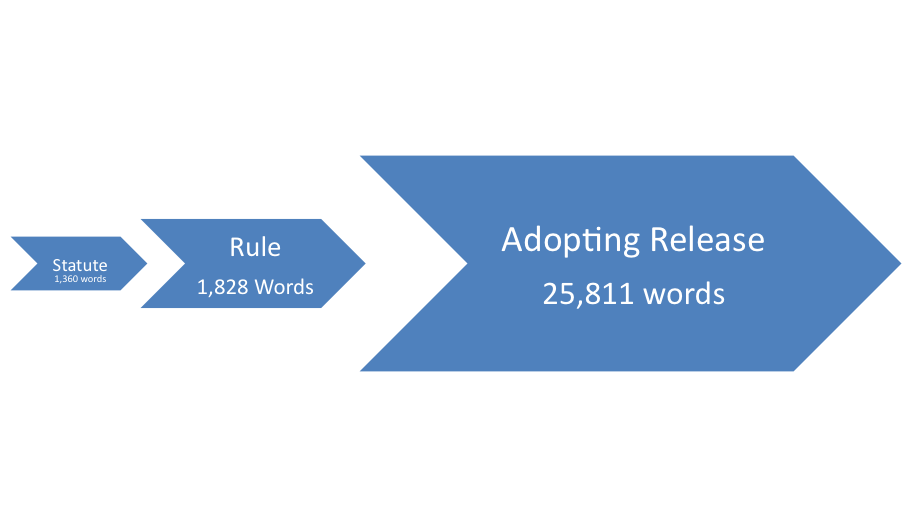

Recently, I commented on the extreme laconism of the SEC's summaries of ex parte meetings involving rulemaking. This contrasts sharply with the SEC's approach to adopting releases in which the number of words used to explain a new or amended rule can far exceed the number of words in the rule itself. I've therefore created what I call the "ARR Ratio" - Adopting Release to Rule Ratio. The ARR Ratio is calculated by dividing the total number of words in the Adopting Release by the total number of words in the actual text of the rule being adopted. In the case of the SEC's new compensation committee rule, I calculate the ratio to be 14.44 (approximately 26,000/1,800). I didn't actually count the words, but used the Word program's word count function. The ARR Ratio illustrates that it took the SEC about 14 times as many words to explain the rule as it did to actually state the rule.

The SEC is not alone in publishing lengthy explanations even though the Administrative Procedure Act only requires a "concise general statement of their basis and purpose". 5 U.S.C. § 553(c). The federal APA (unlike California's) does not explicitly require a response to comments received. Compare Cal. Govt. Code § 11346.9(a)(3) (requiring the agency to include in the final statement of reasons "a summary of each objection or recommendation made regarding the specific adoption, amendment, or repeal proposed, together with an explanation of how the proposed action has been changed to accommodate each objection or recommendation, or the reasons for making no change."). However, the failure to respond to comments may put the agency's decision at risk if challenged in court. See Portland Cement Ass'n v. Ruckelshaus, 486 F.2d 375 (D.C. Cir. 1973) (finding that while an agency need not respond to every comment, an agency's failure to respond or consider comments that "step over" the threshold requirement of materiality is a cause for concern.)

A more pernicious problem can arise when agencies use long statements of basis and purpose to impose requirements that are not found in the rule that is being adopted. The public should be able to read a rule and determine how to comply without reference to the statement of basis and purpose. To bury important regulatory requirements in the adopting release reduces transparency, inhibits compliance and is simply unfair

More on California's Proposed Amendments to Rule 260.204.9

Doug Cornelius recently wrote these comments on California's proposed amendments to Rule 260.204.9 in his Compliance Building blog.

{kind=link}