Title I of the Jumpstart Our Business Startups (aka JOBS) Act amended the Securities Act and the Exchange Act to provide some regulatory relief to issuers that qualify as an "emerging growth company". Recently, the Securities and Exchange Commission adopted various changes to its forms and rules to conform to Title I. The SEC elected not to comply with the notice and comment procedures of the Administrative Procedure Act, finding that for "good cause" that "notice and public procedure thereon are impracticable, unnecessary, or contrary to the public interest". 5 U.S.C. 553(b)(3)(B).

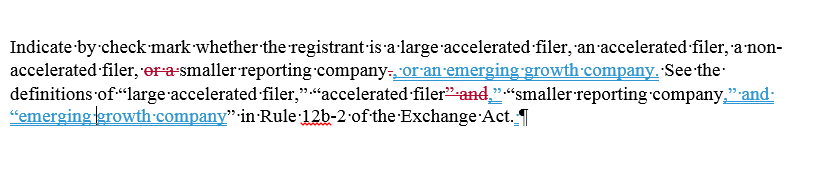

Among other things, the SEC has adopted changes to the cover pages of Forms 10-Q and 10-K. These changes primarily amount to the addition of "emerging growth company" to the check-the-box instruction as indicated below:

(boxes omitted) The SEC has also added the following instruction (and box):

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

My issue is with the first change. The former four categories of issuer (large accelerated filer, accelerated filer, non accelerated filer and smaller reporting company) were mutually exclusive categories. Emerging growth company, however, is not necessarily exclusive. For example, an issuer may be an emerging growth company and an accelerated filer. Because the revised instruction is written in the singular ("check mark", not "check marks") and in the alternative, it implies that only one box should be checked. Perhaps public notice and opportunity for comment might not have been unnecessary after all.

.png?width=100&height=100&name=corporate_law_blogs%20(1).png)