Section 2117 of the California Corporations Code requires every foreign corporation (other than a foreign association) that is qualified to transact intrastate business to file a statement of information. The initial statement of information is due within 90 days of the filing to the original statement of designation. Thereafter, a statement of information must be filed annually "during the applicable filing period". Curiously, however, the statute never states what constitutes the "applicable filing period" or how it is to be determined.

Section 1502 imposes a similar filing requirement on "corporations". As defined in Section 162, these are corporations formed under the California General Corporation Law. However, Section 1502(d) defines the "applicable filing period" as the calendar month during which the original articles were filed and the immediately preceding five calendar months. Why doesn't this definition apply to Section 2117? Section 1502(d) begins with "For the purposes of this section". Thus, "applicable filing period" is quite clearly defined only for purpose Section 1502. Nevertheless, Section 2117(f) provides that subdivisions (c), (d), (f) and (g) of Section 1502 apply to statements filed pursuant to Section 2117.

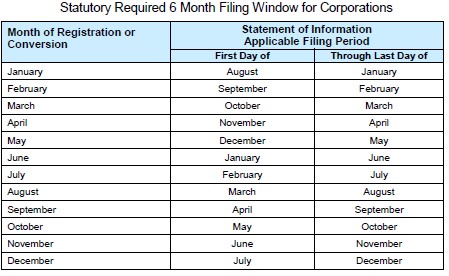

Not surprisingly and perhaps pragmatically, the Secretary of State interprets the "applicable filing period" under Section 2117 as having the same meaning as under Section 1502 and even provides this handy table:

Updated 4/29/2021

.png?width=100&height=100&name=corporate_law_blogs%20(1).png)